Something every property owner needs to understand…

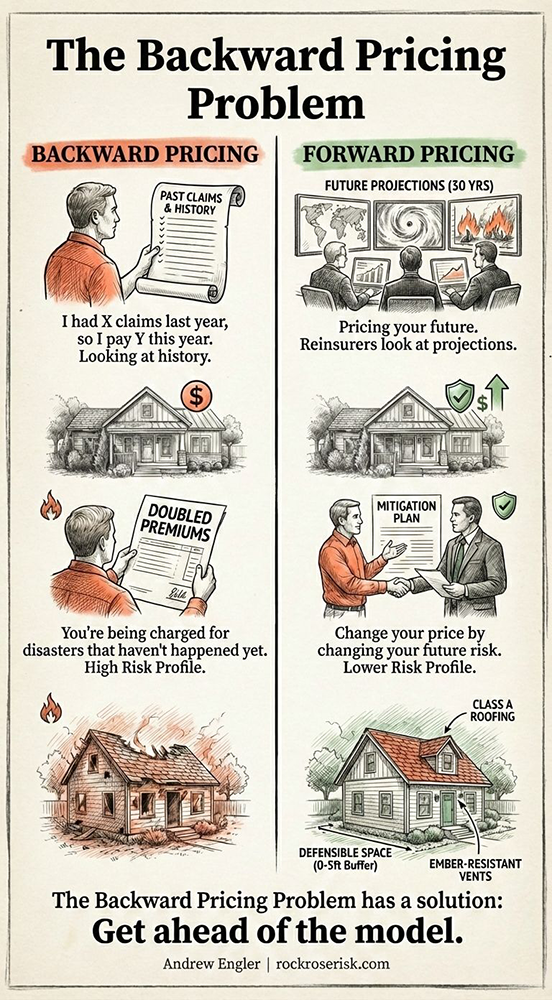

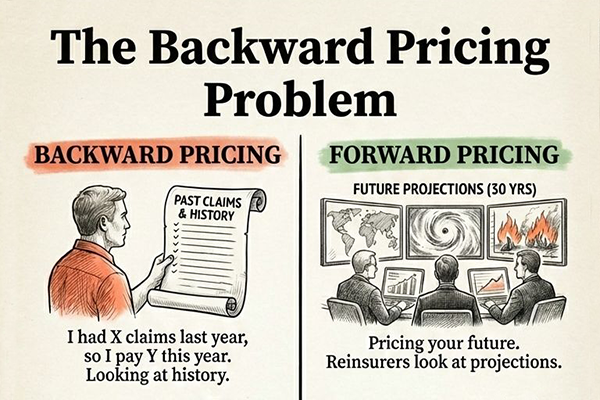

The Backward Pricing Problem.

If your insurance premiums have doubled, this explains why and what to do about it.

Most property owners think insurance works like this:

“I had X claims last year, so I pay Y this year.”

They’re pricing backward. Looking at history. But that’s not how insurance works anymore.

Reinsurers (the companies that insure your insurance company) flipped the model. They’re not pricing your past. They’re pricing your future. A new Wharton study analyzed 74 million premiums and found something stunning:

- Construction costs only explain 35% of premium increases.

- The other 65%? Reinsurers are looking at wildfire and hurricane projections for the next 30 years.

They didn’t like what they saw. So they doubled their prices between 2017 and 2024.

This is the Backward Pricing Problem:

You’re being charged for disasters that haven’t happened yet.

And the “risk-to-premium gradient” more than doubled. If you’re in a high-risk area, you’re paying exponentially more than you were 7 years ago.

Here’s where it gets interesting:

If they’re pricing your future risk, you can change that price by changing your future risk.

Mitigation isn’t a cost. It’s a negotiation with the algorithm that sets your premium.

Every dollar you spend on defensible space, ember-resistant vents, and Class A roofing is a dollar that changes how reinsurers model your property.

Same building. Different risk profile. Different price.

The Backward Pricing Problem has a solution:

Get ahead of the model.

I’ve seen property owners cut premiums by hundreds of thousands by documenting exactly what they’ve done to reduce future risk.

The reinsurers are betting against your property.

The question is: are you going to prove them right, or prove them wrong?

So Cheat the System:

Spend money before you have to.

Sounds backwards. But the math is simple.

$50K on mitigation now saves $400K in premiums over three years. That’s an 8x return. No stock does that.

Most property owners wait until their premium triples. Then they panic. Then they mitigate. Then they wait years for insurers to notice.

The smart ones spend early. Document everything. Show insurers the reduced risk before renewal.

Smart property owners know they’re not spending money. They’re buying leverage.

Proactive spending isn’t an expense. It’s an investment with guaranteed returns.

Smart property owners know they’re not spending money. They’re buying leverage.

Proactive spending isn’t an expense. It’s an investment with guaranteed returns.

Article by:

Andrew Engler

CEO – RockRose Risk

rockroserisk.com